Pandas

Overview

Teaching: 30 min

Exercises: 15 minQuestions

What is Pandas and why should I use it?

Objectives

Creating a pandas DataFrame

Indexing DataFrames

Listing column names of a DataFramePrinting elements of a DataFrame by indexing

Reading in data from a CSV into a DataFrame

Analyzing a DataFrame using built in functions ( df.sum() , df.cumsum() , df.std() )

Pandas is an open source library which provides data structures and data analysis tools for python. You will notice many similarities between Pandas and NumPy because Pandas is built on top of NumPy using and expanding on NumPy’s functionality. At the core of Pandas is the pandas dataframe. Dataframes are similar to multi-dimensional arrays but they include labels and indices which can be of many types including time, simplifying the use of time series data.

Creating DataFrames

The Pandas DataFrame class is used to manage labeled and indexed data much like one would in SQL.

To import the Pandas library do the following:

import pandas as pd

Pandas DataFrame is created with the form:

pd.DataFrame(Data,Labels,Index)

Create and print a Pandas DataFrame with:

df = pd.DataFrame([10,20,30,40],columns=['numbers'],index=['a','b','c','d'])

print(df)

numbers

a 10

b 20

c 30

d 40

The main concepts to take away from a Pandas DataFrame are:

- Data: can be one of the following (list,tuple,ndarray,dict)

- Labels: data organized into columns which can have custom names

- Index: index that can take on different formats (numbers, strings, time information)

We can print out the labels and index of the DataFrame:

print(df.index)

print(df.columns)

Index(['a', 'b', 'c', 'd'], dtype='object')

Index(['numbers'], dtype='object')

We can also initialize a Pandas DataFrame by calling the underlying Numpy function ‘ones’ and wrapping it with a Pandas DataFrame:

df1 = pd.DataFrame(pd.np.ones((3,3)))

print(df1)

0 1 2

0 1.0 1.0 1.0

1 1.0 1.0 1.0

2 1.0 1.0 1.0

We passed the ones function a tuple of (3,3) which will create a 3 by 3 matrix initialized with the values of 1 and then wrap the Numpy array in a Pandas DataFrame. We can also use the zeros function to initialize the DataFrame with values of zero:

df0 = pd.DataFrame(pd.np.zeros((3,3)))

print(df0)

0 1 2

0 0.0 0.0 0.0

1 0.0 0.0 0.0

2 0.0 0.0 0.0

We can append data to the end of our dataframe with append:

df2 = pd.DataFrame([50,60,70,80],columns=['numbers'],index=['e','f','g','h'])

df = df.append(df2)

print(df)

numbers

a 10

b 20

c 30

d 40

e 50

f 60

g 70

h 80

We can add a column to our dataframe by assigning values to it’s label:

df['10x'] = df.numbers*10

print(df)

numbers 10x

a 10 100

b 20 200

c 30 300

d 40 400

e 50 500

f 60 600

g 70 700

h 80 800

Pandas has more ways to concatenate data than we can cover in this workshop. For more information on concatenating data please visit Pandas merging documentation

Indexing DataFrames

Pandas has two primary types of indexing:

.loc: is label and index based:

print(df.loc['a'])

print('----------------')

print(df.loc['a','10x'])

print('----------------')

print(df.loc['a':'d','10x'])

numbers 10

10x 100

Name: a, dtype: int64

----------------

100

----------------

a 100

b 200

c 300

d 400

Name: 10x, dtype: int64

.iloc: is integer position based (from 0 to length-1)

print(df.iloc[0])

print('----------------')

print(df.iloc[0,1])

print('----------------')

print(df.iloc[0:3,1])

numbers 10

10x 100

Name: a, dtype: int64

----------------

100

----------------

a 100

b 200

c 300

Name: 10x, dtype: int64

Importing and Exporting data from CSV files

We can write our dataframe out to a CSV file with:

df.to_csv('numbers.csv')

!cat numbers.csv

,numbers,10x

a,10,100

b,20,200

c,30,300

d,40,400

e,50,500

f,60,600

g,70,700

h,80,800

We can read in CSV data into a DataFrame (AZO.csv):

df = pd.read_csv('AZO.csv')

Note: If an index column is not specified then pandas will create an index column for you starting with 0.

Now that we have data inside of a DataFrame we can look at the DataFrame with a few commands:

print('head\n',df.head())

print('tail\n',df.tail())

head

Date Open High Low Close Adj Close \

0 2017-12-05 747.000000 763.299988 703.599976 712.760010 712.760010

1 2017-12-06 705.630005 711.760010 696.940002 698.650024 698.650024

2 2017-12-07 701.460022 704.090027 693.750000 702.340027 702.340027

3 2017-12-08 702.789978 723.429993 701.289978 721.890015 721.890015

4 2017-12-11 719.590027 720.799988 705.780029 708.609985 708.609985

Volume

0 1225500

1 492900

2 417300

3 546900

4 501900

tail

Date Open High Low Close Adj Close \

247 2018-11-28 835.380005 840.650024 826.599976 833.700012 833.700012

248 2018-11-29 835.530029 836.739990 824.020020 825.830017 825.830017

249 2018-11-30 827.090027 827.090027 804.570007 809.070007 809.070007

250 2018-12-03 814.049988 829.710022 807.059998 824.460022 824.460022

251 2018-12-04 867.099976 894.369995 854.500000 880.070007 880.070007

Volume

247 349900

248 279200

249 602900

250 535700

251 935200

Working with Dataframes

There is a large variety of functions that pandas provides for Dataframes. View Pandas API reference for documentation. In this workshop we will review a few of them to give you an idea of their potential:

DataFrame.sum() Sum the values on the requested axis (default is columns):

print(df.sum())

Date 2017-12-052017-12-062017-12-072017-12-082017-1...

Open 180132

High 182133

Low 177975

Close 180038

Adj Close 180038

Volume 92264300

dtype: object

DataFrame.cumsum() Return the cumulative sum of the requested axis:

print(df['Close'].cumsum().head())

0 712.760010

1 1411.410034

2 2113.750061

3 2835.640076

4 3544.250061

Name: Close, dtype: float64

DataFrame.std() Return the standard deviation of the requested axis:

print(df.std())

Open 59.753627

High 60.613944

Low 59.501632

Close 60.590288

Adj Close 60.590288

Volume 208536.419569

dtype: float64

Economic example using Pandas

Let’s repeat the example from NumPy using Pandas, this time using the file AZO.csv which includes time data

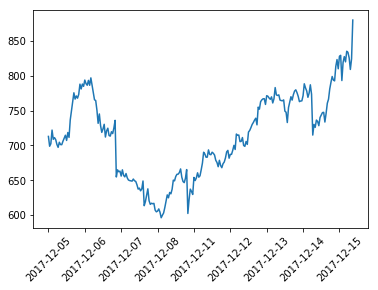

Load the file using pd.read_csv and plot just the adjusted close values:

Note: There are a few extra commands included here to format the plot and make the dates visible. Don’t worry if you don’t understand them now, we will cover more about matplotlib later

import matplotlib.pyplot as plt

# simple function to format plot to make the dates legible

def plot_dates(df):

fig, ax = plt.subplots()

plt.plot(df)

ax.set_xticks(df.index[0::30])

plt.xticks(rotation=45)

plt.show()

# read the data in and plot it

data = pd.read_csv('AZO.csv', index_col=0)

plot_dates(data['Adj Close'])

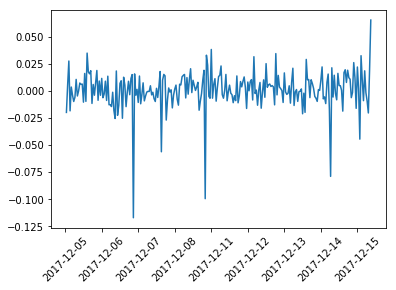

Next we’ll calculate the log returns and plot them, this time using a pandas dataframe function called pct_change(). We could use the same NumPy method for calculating the log returns, but using the pandas function we keep the indices for the data (dates)

import numpy as np

log_returns = np.log(1 + data['Adj Close'].pct_change())

plot_dates(log_returns)

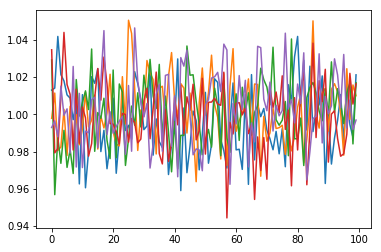

Next calculate the mean (u), variance (var), Standard deviation (std) and drift (drift) the same way we did with NumPy

u = log_returns.mean()

var = log_returns.var()

std = log_returns.std()

drift = u-(0.5*var)

Say we want to run 5 simulations predicting the next 100 days of returns. First generate a 2 dimensional array of random values of size (100,5), just like we did with NumPy:

rand_vals = np.random.rand(100, 5)

print(rand_vals.shape)

(100, 5)

Next with some help from SciPy’s statistical library let’s calculate the percent point function using our random values:

from scipy.stats import norm

ppf = norm.ppf(rand_vals)

Calculate the daily returns using the results of our previous step and plot them:

returns = np.exp(drift + std*ppf)

plt.plot(returns)

plt.show()

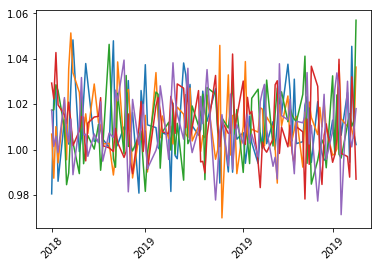

Next with some help from Pandas we will determine what the next 100 business days are and merge set them as the indices for our daily returns

from pandas.tseries.holiday import USFederalHolidayCalendar

from pandas.tseries.offsets import CustomBusinessDay

us_bd = CustomBusinessDay(calendar=USFederalHolidayCalendar())

prediction_dates = pd.date_range(start=data.index[-1], periods=100, freq=us_bd)

returns_dates = pd.DataFrame(returns,index=prediction_dates)

plot_dates(returns_dates)

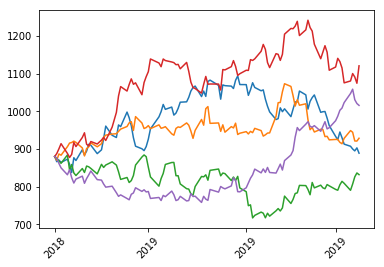

Convert this back to daily stock values by creating an empty dataframe the same size as our returns with our prediction dates as the indices and assign the first row (starting values) to be the same as the last row in our initial data set. Then loop through our data calculating the daily values and plot it

predictions = pd.DataFrame(np.zeros(returns_dates.shape),index=prediction_dates)

predictions.iloc[0] = data['Adj Close'].iloc[-1]

for i in range(1,predictions.shape[0]):

predictions.iloc[i] = predictions.iloc[i-1]*returns_dates.iloc[i]

predictions.head()

plot_dates(predictions)

Challenge

Using the predictions from above pick a date and print the predicted stock values for all 5 predictions for that date

Solution

print(predictions.loc['2018-12-26'])0 897.879181 1 914.058514 2 859.522983 3 923.701527 4 817.625782 Name: 2018-12-26 00:00:00, dtype: float64

Key Points

What are Dataframes

Using dataframes